The first quarter of 2026 started off as a continuation of 2025, but in late February markets took a turn. That turn has more or less reversed itself over the past several weeks, but uncertainty has increased.

In equity markets, large US stocks lagged both smaller US and foreign equities. The S&P 500 fell over 4%, while other benchmarks were flattish to slightly down. We note that the drawdown was greater outside the S&P 500. Smaller US and foreign stocks broadly had started the year off on a much stronger note, but in most instances gave it all back. The early year rally was broad, but the sell-off was equally broad.

The bond market was also slightly lower on the quarter, inclusive of the interest accruals as interest rates ticked higher. Riskier bonds were also lower, but not meaningfully so. In our view, this is a modest surprise. The financial media spent much of March, and now April, focused on the emerging trouble in something called private credit and the difficulties various private credit funds had in meeting redemption requests from their investors. We expand on that topic and share some thoughts on the asset class later in this note.

The Iran Conflict

As far as the market broadly is concerned, the US conflict in Iran appears to be the primary focus. Markets sold off as the US began to actively pursue changes to the status quo with military intervention. We view the reaction function that drove markets as increased uncertainty, higher oil prices leading to higher expected inflation, a yield curve that rose in response, and a potentially longer path to lower short-term interest rates from the Federal Reserve. In light of that potential chain of events, it is fair to say recession probabilities are higher to some degree. However, the actual probabilities before and after the events in Iran are unknowable and simply forecasts. We also note that, as this situation unfolds, the facts and circumstances have a way of changing and evolving quickly.

Private Credit Market Issues

Within markets, we mentioned that private credit concerns are also driving some of the volatility. It is worth describing this area, why it has grown so much, what has so many commentators concerned, and sharing some observations.

Private credit is an offshoot of private equity. It emerged after banking regulations following the Great Financial Crisis made it more difficult for certain companies to obtain loans from banking institutions. Borrowers themselves are typically smaller and private companies. The loans tended to be more expensive for the borrower, but much easier to obtain. Interest rates were typically higher because the individual borrowers are considered riskier. Lenders packaged these loans up into portfolios and, in theory, reduced the risk because the portfolio can be considered diversified. Pensions, endowments, and family offices invested on the idea that these portfolios offered higher returns with reduced risk. Over the past several years, the private credit sponsors have expanded their market by offering vehicles to high-net-worth individuals. Up until the past several quarters, marketing efforts were very successful. This has been an area of significant inflow and high growth in the asset management industry.

Private credit investing comes with some tradeoffs, some of which may be worth it to the right kind of investor. The most notable one is illiquidity. These loans are typically held to maturity, and the secondary market for a manager looking to exit is limited. Funds typically offer some liquidity to investors but have the ability to restrict redemptions if too many investors ask for too much of their investment back. This is what many of today’s headlines are highlighting, as many investors have asked to redeem their interests and are only getting a portion of their investment back.

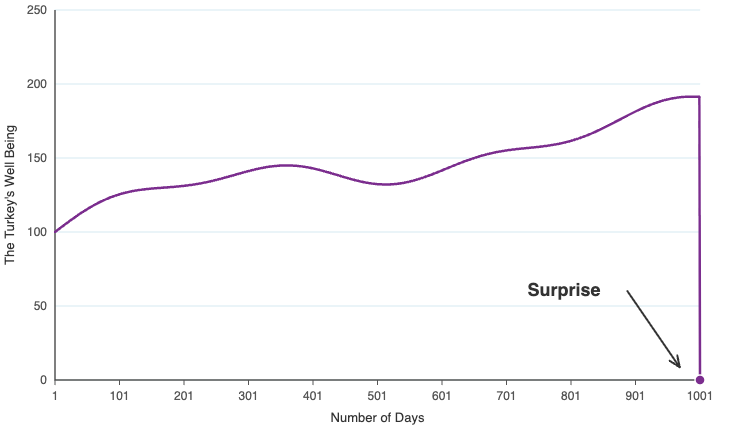

The second tradeoff is how and when the loans get valued. Firms use providers to value and/or validate their valuations, but the portfolios are marked to a financial model, not the market. There are instances where different firms, owning slices of the same loans have different valuations. Private credit loans are also getting valued less frequently than instruments that have frequent open market transactions. Recently, there have been instances where loans were valued near par, only to see them marked down to pennies on the dollar when a credit event surfaces. We are reminded of Nassim Taleb’s “Black Swan” turkey chart.

How many private credit loans are living the life of a Thanksgiving turkey? No one really knows. For investors, the lack of volatility is a byproduct of the valuation practices, but the risks do not disappear simply because the valuations appear stable.

Lastly, private credit has not been through a prolonged negative credit cycle. The sponsors insist they have protections for investors and have conducted thorough due diligence on the borrowers they lend to. Absent evidence to the contrary, it seems reasonable to take them at their word and assume they believe this. However, given the growth the space has experienced, it seems fair to question whether it is possible to lend so much money in such a short period of time and not have credit quality suffer. We also wonder what could happen to default rates and recoveries for investors in a prolonged credit crunch. Time will tell.

Our view is that the issues in private credit are not systemic, but potential for some spill-over is real. The loans are held to maturity in most cases, but many borrowers are unlikely to repay loans at maturity without a new loan taking its place. There is risk old loans do not get refinanced into new loans, a risk that increases with redemption requests from investors. As that occurs, private credit investors could learn their loan portfolio has increasingly become a private equity portfolio. Institutions and wealthy investors might not get access to their capital and/or suffer negative marks, but this in and of itself is not a tragedy.

One might wonder, if this is all happening in private markets, what this may mean for public markets. Private credit is funding, to an unknown degree, the AI data center buildout. To the extent private credit pulls back, either out of desire or necessity, it could negatively influence the AI capex cycle that has been driving markets. How much so is unknowable and remains to be seen.

Final Thoughts

So far, markets have staged a comeback in April. The ups and downs seem to be driven by the latest developments in Iran. We hope the conflict is short and resolved to the satisfaction of the parties soon, but uncertainty remains elevated. It is helpful to remember that in markets and the economy that more things can go wrong than do.