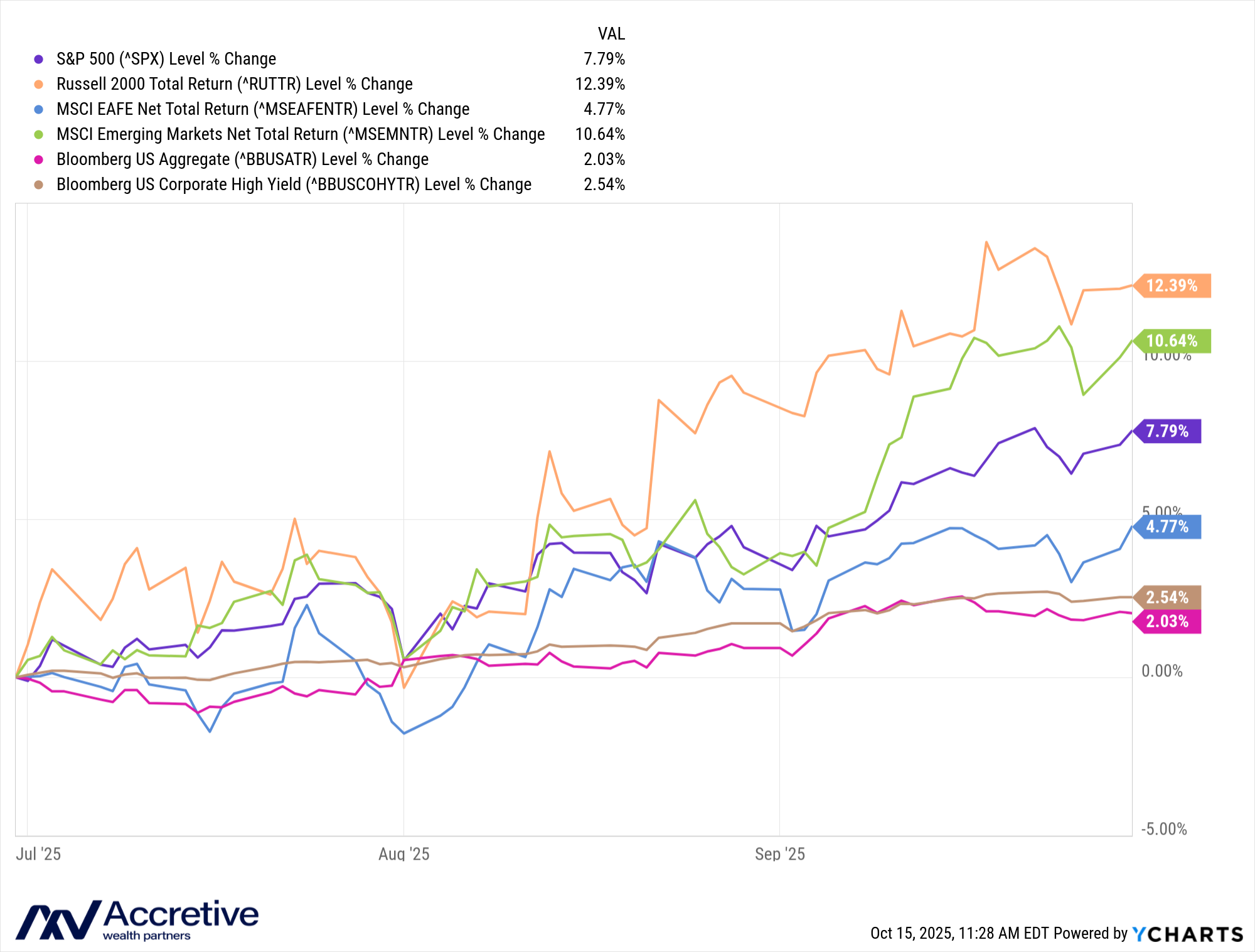

The third quarter was strong for markets and asset prices.

Equity prices continued to recover from the tariff related sell-off that occurred earlier this year and make new highs. The melt-up over the last several months has largely been led by the AI trade. The market’s attitude relating to non-AI stories has been more rational in general and in some ways apathetic.

The bond market was also higher as interest rates ticked modestly lower and capital markets remained healthy. After much cajoling from the White House, the Federal Reserve cut the benchmark Fed Funds Rate by 0.25% in September and projected more to come in subsequent meetings, assuming economic conditions continue to justify some easing. We think the key conditions, as far as the Fed is concerned, are inflation, inflation expectations, and the labor market. Looking at the data, it seems the labor economy has some underlying weaknesses. Absent a meaningful uptick in inflation, possibly from the tariffs flowing through to the economy, it seems reasonable to expect a bit more easing over the coming months.

At a high level, the US economy seems to be holding up. Growth has been acceptable, but beneath the surface it is really a “K” shaped economy. Most of the growth has been attributable to investment in AI. Absent AI investment, economic growth has been slow. We note that this is despite a federal government that is still running historically high budget deficits.

With respect to AI, the enthusiasm has bordered on euphoria. OpenAI (which is not a publicly traded company, yet) has been announcing numerous partnerships and deals, along with ambitious plans. Most recent estimates of OpenAI’s revenue come in at about $13 billion, while their spending plans over the next 5 years top $1 trillion. Publicly traded companies are being rewarded by the market for announcing massive capital spending plans and initiatives.

Up until this year, a lot of the capital spending has been funded with cash flows from operations of the largest tech companies (the “MAG-7”). That is still occurring, but the scale of the spending is consuming abnormally high proportion of their cash flows. The attitude is that they are more willing to risk overspending rather than risk being left behind.

As of late, we think it is fair to say the financing of these projects is getting more creative, clever, and opaque. Companies are tapping various debt markets and creating special purpose vehicles in order to get them off their balance sheet. There are also a variety of complex business arrangements that make one wonder who is buying what and from whom. The opportunity for something to go wrong, even if that something is just mal-investment, seems to be growing alongside the enthusiasm.

Commentators are comparing the investment cycle to the laying of the internet in the 1990’s and the railroad boom of the late 1800’s. The scale of the investment seems comparable, but there are differences. The useful life for much of the capital expenditure is only a few years (best estimates are 3-5 years for chips) instead of decades for fiber and rail. The return on this spend in many cases is still “TBD”, but the nature of the assets requires massive ongoing spending to maintain (and probably increased spending to stay on the leading edge). We think it is fair to say this will continue if companies are being rewarded by the market for their spending plans. We wonder how long investors will reward companies for massive spending plans without a commensurate return on that investment or if the harvest period for those returns is too short. A lot is at stake, as most of the GDP growth in the United States is currently dependent upon it.