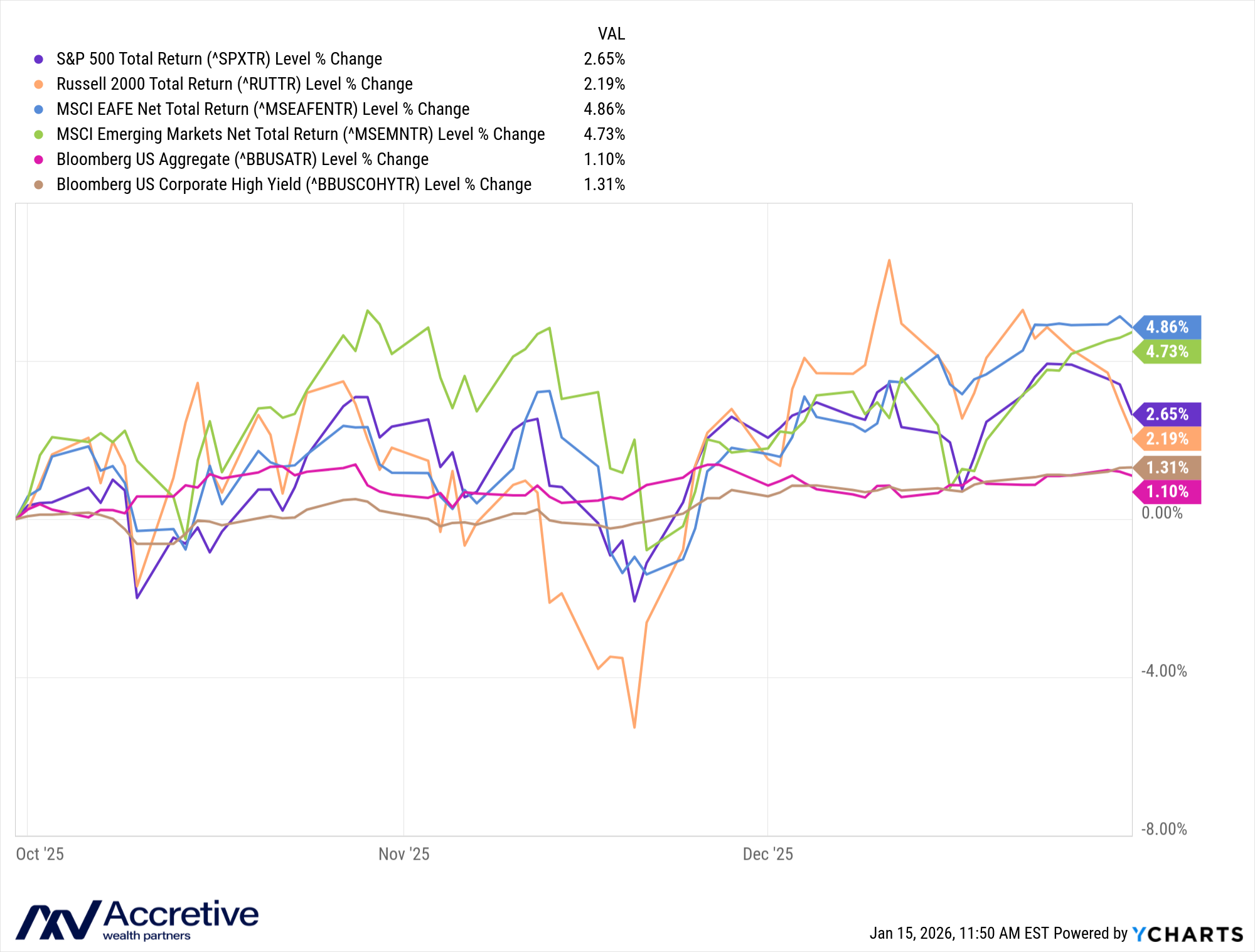

In many ways, the fourth quarter was a continuation of the third, as the market continued to grind higher.

In equity markets, foreign stocks outpaced domestic stocks, as they rose a bit more and the dollar continued to weaken. In the US, large and small companies rose comparable amounts. In general, the market has climbed a wall of worry and shaken off a variety of potential shocks and uncertainty.

The bond market was also higher on the quarter, but it was mostly driven by yield accretion, rather than meaningful moves in interest rates on the longer-end of the yield curve. The environment for riskier borrowers remained relatively calm, though there was some notable distress in the quarter. Whether that distress spreads or is indicative of a turn in the cycle remains to be seen.

The Fed cut short-term interest rates twice in the fourth quarter and signaled another cut coming sometime in 2026. Voting within the Fed was notable because, for the first time in a while, there was meaningful dissension among the voters. Several members voted against cuts, while one member argued for deeper cuts. The market seems to think at least two cuts are coming this year. These forecasts are just informed guesses, but the direction of short-term rates appears to be heading downward some from here.

In prior notes, we wrote about the prospect of Fed independence being challenged by the administration. That prospect now appears to be reality. The President favors lower short-term rates, and the administration has put unprecedented amounts of pressure on both the Fed and its chairman, Jerome Powell. From our perspective, whether we like it or not, the administration is likely to get what it desires eventually, as there will be a new Fed chair when Jerome Powell’s term ends in May.

In our last update, we wrote about the “K” shaped economy. Not much about that has changed, but we think if short-term rates move lower outside a recession scenario, economic growth could be a bit less “K” shaped.

Last time we wrote about the AI investment cycle; much of it remains the same, and you can read our prior post on it here.

As we look into 2026, the AI investment cycle seems poised to continue, but returns on that investment are still “To be determined”. As the return on investment picture becomes clearer, that may create challenges for valuations and project-funding. The rest of the market does not appear to have the same enthusiasm priced in, but we note that tech has become a very large part of the market. The prospect of lower borrowing costs and tax-reform provide something of a tailwind, while tariffs and a tepid employment outlook are potentially a bit of a headwind.

The day-to-day news flow can make an investor’s head spin. We remind clients and readers to keep their focus on the long-term, both for the market and their financial objectives.